Cracks are beginning to appear in how consumers handle their debt as higher costs of living and inflation take a toll on consumers—and they're most pronounced among younger borrowers.

We've analyzed Federal Reserve Bank of New York data to illustrate how different generations handle debt payments amid higher prices and high interest rates.

While it may seem counterintuitive, debt can be a useful tool. It allows consumers to bridge financial gaps in an emergency or invest in a home with the cash they have today. When debt is paid off consistently and on time, it helps consumers build good credit, which qualifies them for better interest rates on car loans, mortgages, personal loans, and more.

However, debt can be tricky to navigate for consumers.

Managing debt can be empowering when it helps build wealth and financial stability. But particularly for young people just getting their financial footing, being saddled with debt can quickly become overwhelming. People under the age of 30 are still early in their professional lives. They typically have less financial security than more established generations with decades of earnings under their belts. They are also more likely to rent than own their home, exposing them to annual housing cost increases that put a dent in savings plans.

These factors can make debt more appealing to take on and less feasible to pay off, impacting their financial wellness for years to come.

The Gen Z and millennial generations also face unique financial challenges. They're likelier than other generations to spend time online, where studies have shown social media platforms like Instagram can warp their sense of financial success, dubbed "money dysmorphia." A 2023 Qualtrics/Intuit Credit Karma survey found that 43% of Gen Z and 41% of millennials experience this phenomenon.

Other studies have found that social media can influence consumers to spend beyond their means. A 2023 Edelman Financial Engines report found about one-quarter of all consumers feel less satisfied with the amount of money they have because of social media, and one-third said they've spent more on something than they could comfortably afford to keep up with the lifestyles portrayed on social media.

When younger consumers overextend themselves financially, they're more likely than older generations to work extra hours or take on extra jobs to pay off those expenses, according to a 2024 Bankrate study. However, when borrowers fall behind on making minimum debt payments, they become what's referred to by lenders as delinquent.

Being behind on payments for one to two months can incur additional late fees and impact credit scores. After three months, the account is considered "seriously delinquent," and the lender can begin repossession, foreclosure, or some other legal action, per credit bureau Experian. Beyond that, lenders may send your account to a collection agency to recoup the money owed.

An uptick in late debt payments reverses a decade of decline following the Great Recession

Overall, seriously delinquent debts in almost all forms tracked by the Fed are up in 2024 compared to 2023, including auto loans, credit cards, and mortgages, continuing a trend that began in 2021. The only kind of debt where delinquencies aren't rising is student loans, according to Fed data.

That's likely due to the Department of Education pausing reporting of delinquent accounts. After a three-year break on student loan repayments, nearly half of student loan borrowers of all ages still haven't restarted payments since the pandemic-era moratorium ended in October of last year, according to a New York Times analysis of Department of Education data.

Borrowers aged 34 and younger represent about half of all borrowers, meaning millions of young people could face negative repercussions when reporting restarts in October 2024.

For now, credit card debt has the most significant impact on young people's financial future.

Roughly 1 in 10 working-age Gen Zers are 3 months or more behind on credit card payments

Over 10% of credit card users between 18 and 29 are seriously delinquent on their credit card payments, a rate that now surpasses the pre-pandemic level. The age group mostly encompasses working-age Gen Z consumers, who have a median credit limit of $4,500 and are more likely than older generations to have maxed out their credit, according to a Fed report published earlier this year.

Close behind those borrowers are younger millennials aged 30-39, with similarly high delinquent credit card debt rates.

Since credit card delinquencies have ticked upward, interest rates have also increased to historically high levels for borrowers. The typical interest rate on commercial credit cards where users paid interest was 22% in May, the latest month for which data is available.

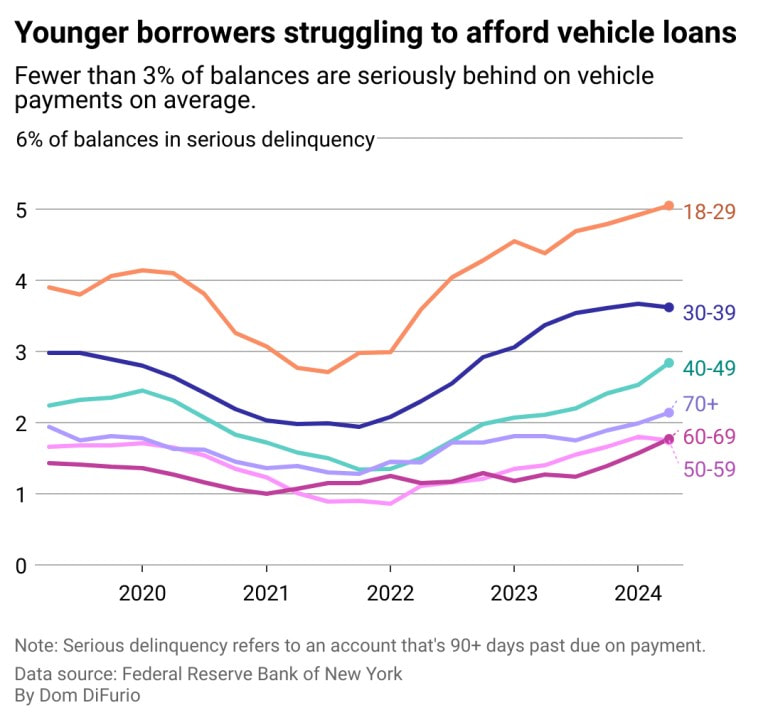

Interest rates on auto loans hitting borrowers under 40 hardest

Young borrowers are also falling behind on vehicle loans at the highest rates of all age groups. It's a trend that's held for some time when broken down by age. Today, however, 5% of loans owned by consumers aged 18-29 are at risk of resulting in repossession, up from fewer than 4% pre-pandemic.

Purchasing new vehicles was never affordable for most young people, but almost everything having to do with owning a vehicle—whether new or used—has gotten more expensive in the last few years.

The typical interest rates for new vehicles ballooned after the Federal Reserve began raising interest rates to combat inflation in 2022. Today, a six-year auto loan carries a typical interest rate of 8.3%, roughly double what consumers were used to in the 2010s.

On top of interest rates, the cost of new and used vehicles has also increased in recent years, though used vehicle prices have come down considerably from their 2022 peak. And car insurance premiums are skyrocketing this year to boot. They jumped 24% on average in 2023 and Insurify projects they will increase a total of 22% this year.

That unaffordability is beginning to show up in credit applications at dealerships and financial institutions, which are rejecting more customers than at any time in the last decade, according to Fed data. Nearly 1 in 5 consumers who applied for an auto loan were rejected in June.

Story editing by Alizah Salario. Additional editing by Kelly Glass. Copy editing by Kristen Wegrzyn. Image via Canva.